So here we are, staring at headlines that whisper of a potential Russia–Ukraine peace deal, and useless sell-side analysts that appear on CNBC daily, looking for any excuse to backfit their evergreen “buy” ratings to some type of good news that can continue to explain 40x PEs and an S&P 200,000 target are salivating.

The narrative is obvious: peace means stability, stability means growth, and growth means stocks go higher. But anyone with more than a week’s experience in markets knows how this script can actually end: not with a euphoric rally, but with a “sell the news” thud. Markets don’t run on world peace; they run on liquidity. Take Covid for example: everyone thought the bubonic plague had landed and all life as we knew it was going to stop — so naturally the NASDAQ tripled off its lows after the Fed firehosed trillions in liquidity to the nation’s uber-rich.

I joked at the time: “The year is 2030. All mankind has died from Covid. A lone server in the basement of the New York Fed continues to bid the Dow to all-time highs.”

So now, if peace gets priced as “the last bullish catalyst,” then what’s left to keep this mania levitating? Has anyone that calls themselves a contrarian thought of the removal of war headlines becoming he trigger for a reversal?

Make no mistake, a reversal is overdue. I know, I know — there’s no point in reminding anyone again, because it feels like the market is never going to go down. I’ve been wrong before, loudly, and on more than one occasion (sometimes the only thing my calls crash are my own P&L). But I also know that when the data screams “bubble,” ignoring it usually doesn’t end well.

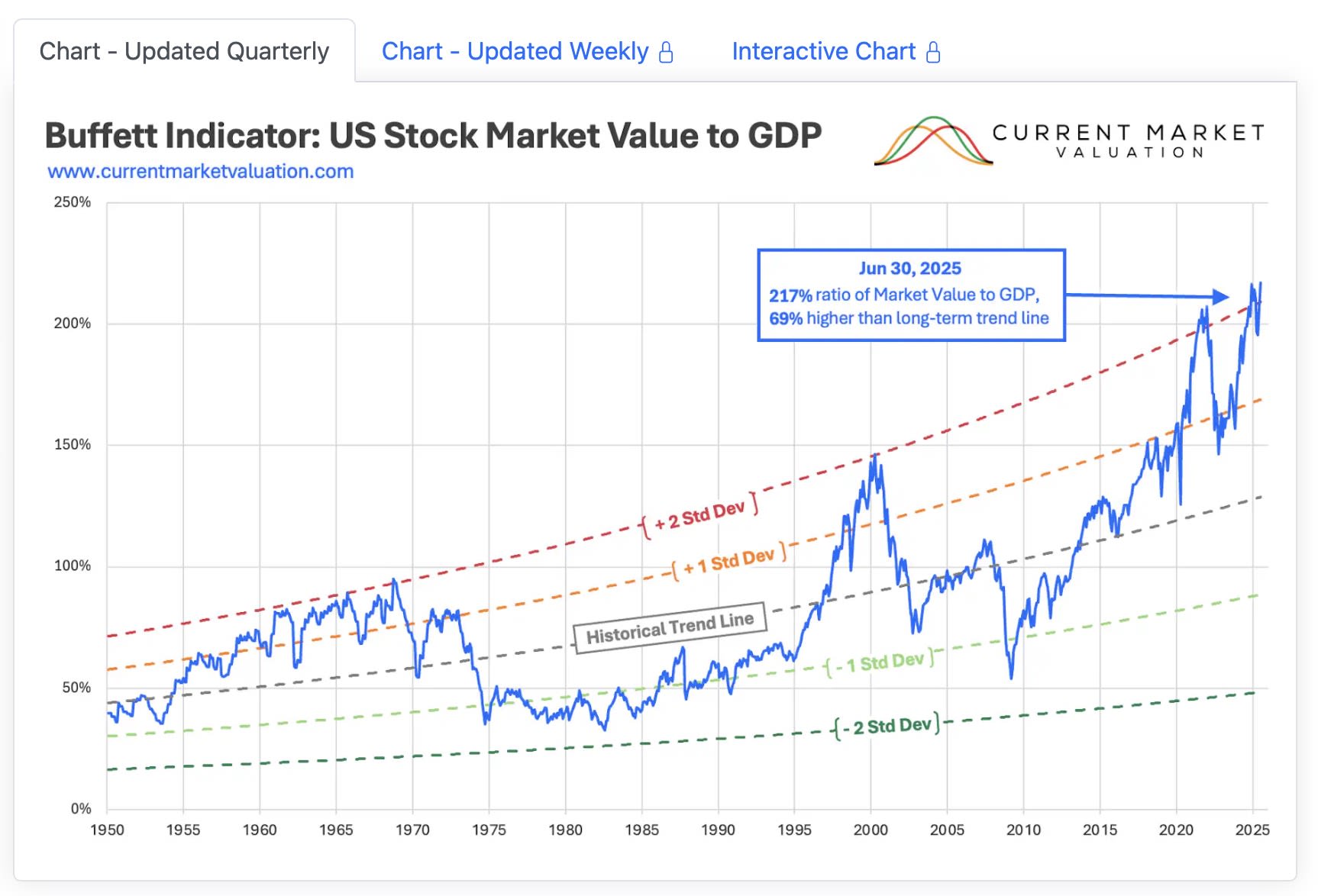

On almost every objective measure, the market is not just expensive — it’s wildly overvalued. June 30th data from CurrentMarketValuation.com doesn’t just say “overvalued” — it says “strongly overvalued,” and it says it across nearly every single model that matters.

Take the Buffett Indicator. It’s sitting around 200% of GDP, more than two standard deviations above its long-term average. The last two times it got anywhere near this level were the dot-com peak in 2000 and again in late 2021. In both cases, investors were treated to drawdowns north of 40%.

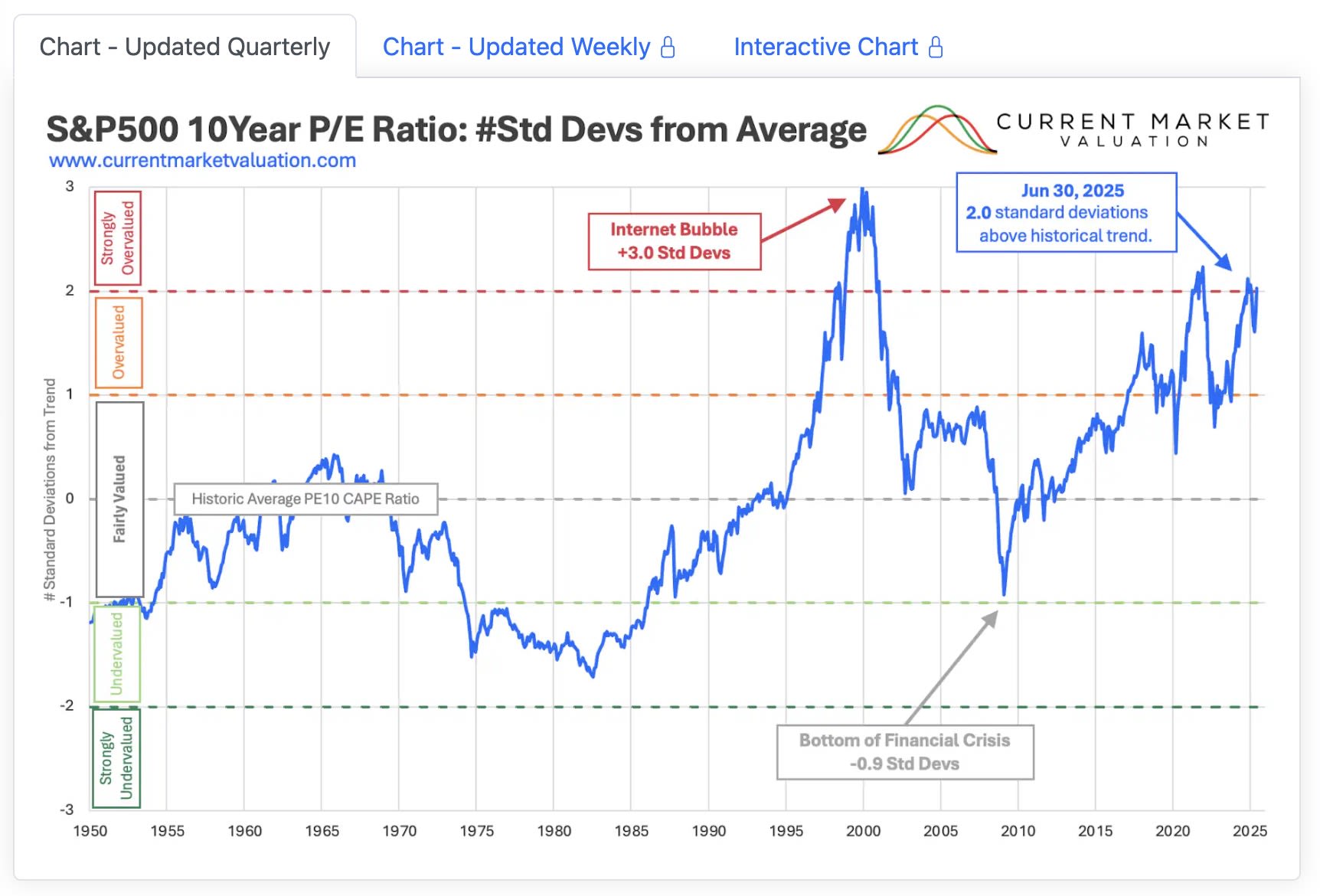

The CAPE ratio tells the same story: hovering in the mid-30s today, more than two standard deviations above its mean. The only other times it has reached these levels were 1929 and 2000 — and we all know how those chapters ended (spoiler: not with soft landings and champagne).

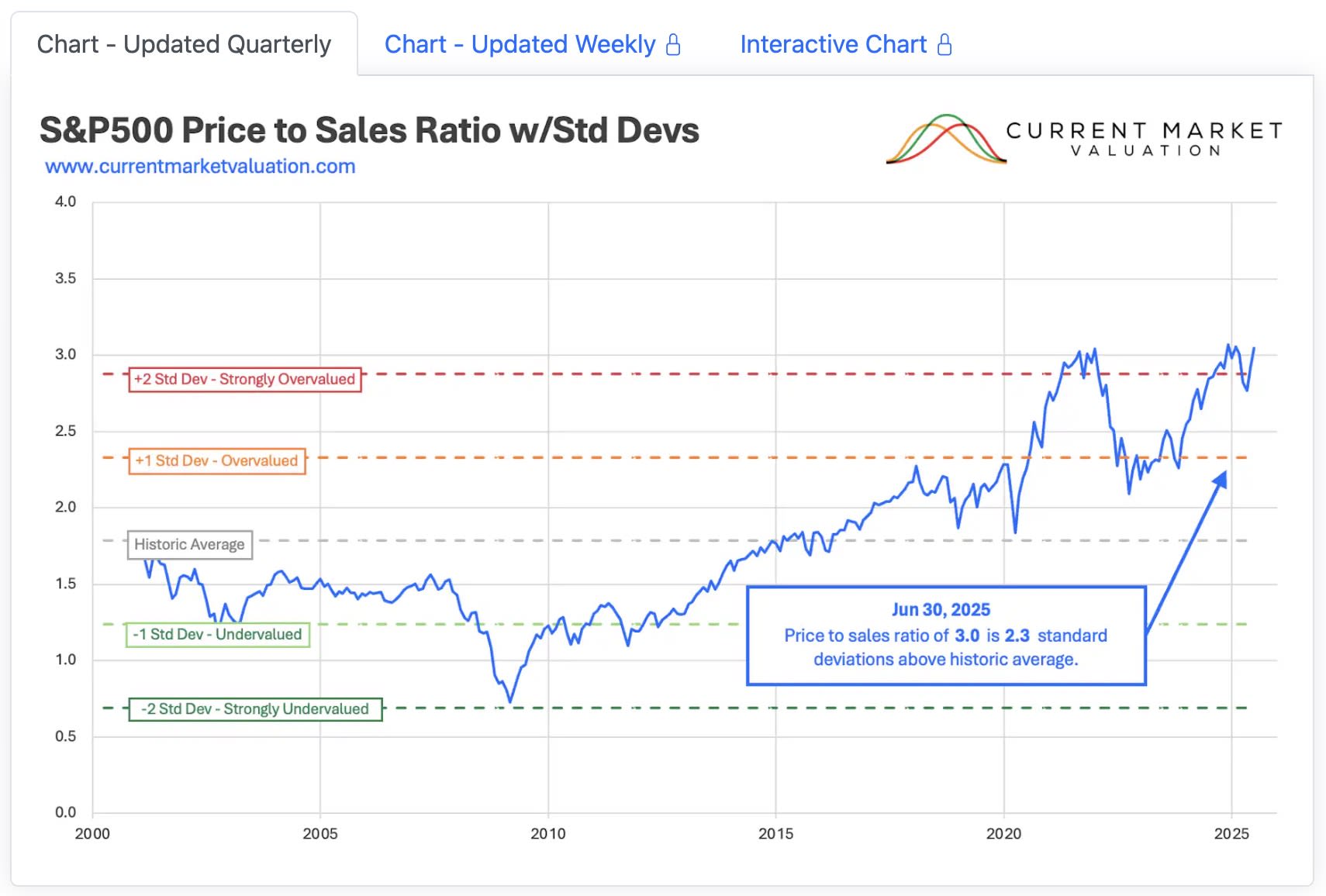

The price-to-sales ratio is equally stretched. At more than three standard deviations above trend, the market is literally off the charts. That level of multiple expansion has never been sustained. Every time it’s gotten this far — whether 2000 or 2021 — it has unwound violently.

The mean reversion model, which plots the S&P 500 against its inflation-adjusted exponential trend line, has the index more than three standard deviations above where history says it should be. The last time it hit that level? Late 2021 — right before a 25% drawdown in 2022. The last time before that? 2000, which needs no introduction.

Even the interest rate model, which usually gives the market a break when yields are low, is flashing red. With the 10-year Treasury yield above 4% and the S&P 500 sitting near record highs, the model calls equities “overvalued.” Translation: even with rates this high, stocks aren’t cheap relative to bonds. The only metric not screaming bloody murder is the earnings yield gap model, which is “fairly valued.” But “fair” in this context means equities are simply less outrageously expensive compared to Treasuries — which sold off with equities on the last pullback — not that they’re a bargain.

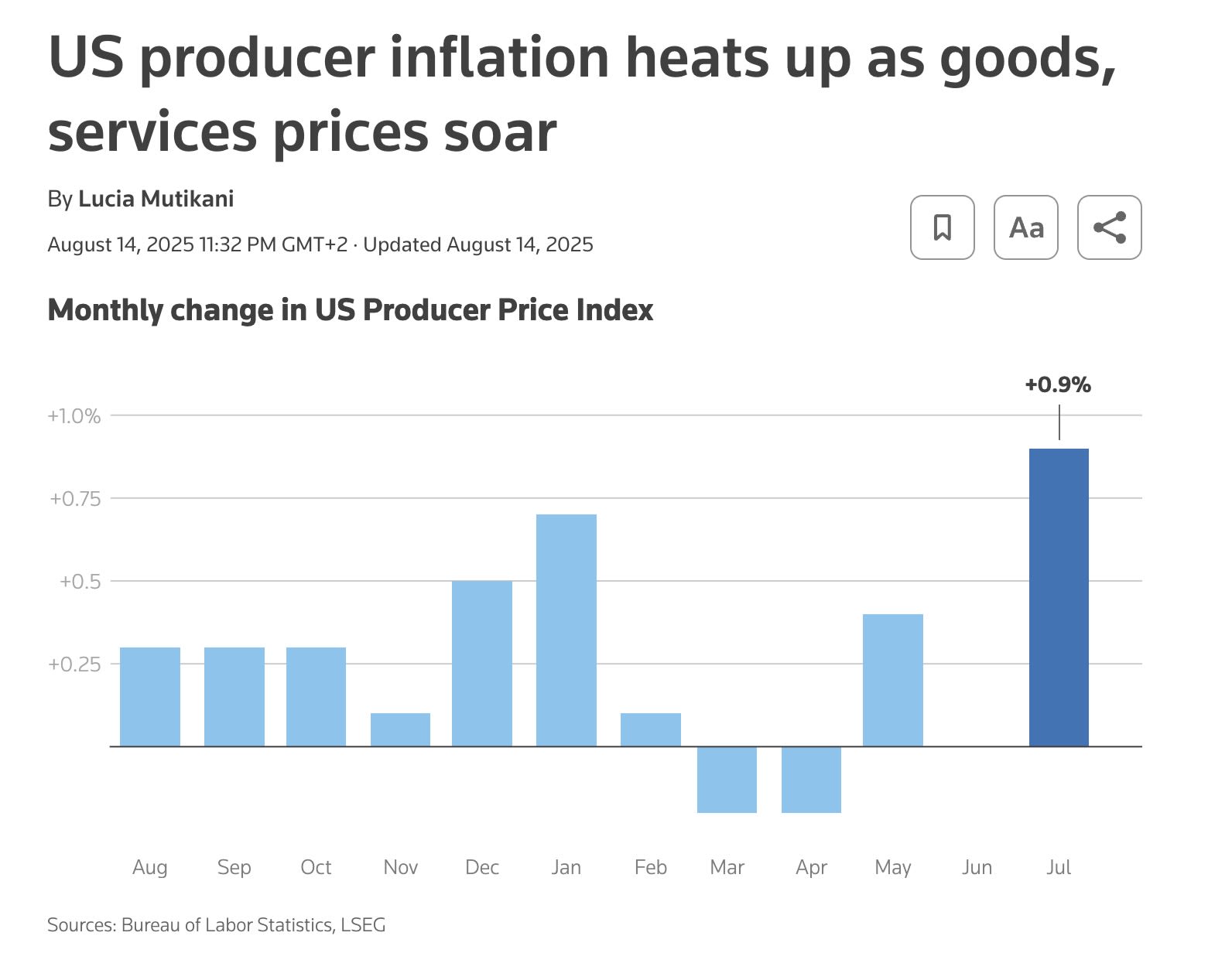

And all of this is happening as macro conditions worsen. The latest PPI report showed producer prices running hotter than expected.

That makes it tough for the Fed to cut rates anytime soon. Positive real rates are grinding the economy to a halt slowly but steadily in the background, a drag that doesn’t show up in day-to-day stock charts but eventually bleeds into earnings. Once earnings estimates get revised down — as they inevitably will if rates stay high and costs keep creeping up — today’s stretched valuations get even worse. Expensive becomes unconscionable.

That’s when a feedback loop kicks in: weaker earnings mean weaker hiring. Job losses follow. And job losses are where my warnings about the passive bid come into play.

Retirement accounts are now north of $40 trillion, and thanks to auto-enrollment and target-date defaults, much of that is funneled into index funds whether or not valuations make sense. Passive has overtaken active management, and the big three firms — Vanguard, BlackRock, State Street — collectively control tens of trillions. Their flows don’t analyze; they just buy. The bigger the stock, the bigger the allocation. That’s how the Magnificent Seven levitate while market breadth gasps for air.

But those inflows depend on payrolls. When jobs go, contributions dry up, and redemptions accelerate as people tap savings. And here’s the dirty little secret: these funds don’t keep giant cash cushions. To meet redemptions, many have already been borrowing against credit lines instead of liquidating assets. That’s leverage by another name. It works when redemptions are small, but if they build, funds flip into forced sellers at the worst possible moment. This isn’t a side pocket of the market — it’s more than half of U.S. fund assets, wired directly into retirement accounts. Which is why I’ve argued that job losses are the silent tripwire. When payrolls crack, the passive bid cracks, and when the passive bid cracks, the market has no floor.

Now, overlay this with crypto — the most volatile risk asset of them all — which is now embedded in the plumbing of the financial system.

I’ve written before about Bitcoin’s “crossing the moat.” It’s no longer knocking on the door; it’s inside the castle, in 401(k)s, ETFs, and corporate treasuries. That integration means a sharp drawdown in crypto wouldn’t just be a sideshow like during the “crypto winter”— it would be a systemic shock. In 2000, it was dot-com stocks. In 2008, it was housing. Today, it could easily be crypto that tips the first domino.

History tells us how this movie ends. When valuations are this far above trend — 1929, 2000, 2008, 2021 — the aftermath isn’t gentle mean reversion. It’s collapse. And every collapse has its catalyst. Maybe it’s a crypto unwind. Maybe it’s the Fed boxed in by inflation. Maybe it’s BRICS announcing a commodity-backed settlement system. Maybe it’s peace in Ukraine, perversely, removing the last bullish narrative. Maybe it’s simply the economy slowing under the weight of positive real rates until earnings crumble. The point is, with valuations this stretched, the catalyst doesn’t matter. The conditions are already there.

And when it comes, it won’t be a glide lower. On the way up, markets climb the stairs. On the way down, they take the elevator. This market has been walking stairs for more than a decade. The elevator shaft is right below it. And sure, maybe I’ve been the idiot standing by that shaft waving “watch out” while everyone else keeps partying upstairs. But history’s pretty clear about how gravity works — even if timing it has always been my personal curse.

Have a great week ahead. Smoke if you got ‘em.

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.

Click this link for the original source of this article.

Author: Quoth the Raven

This content is courtesy of, and owned and copyrighted by, https://quoththeraven.substack.com feed and its author. This content is made available by use of the public RSS feed offered by the host site and is used for educational purposes only. If you are the author or represent the host site and would like this content removed now and in the future, please contact USSANews.com using the email address in the Contact page found in the website menu.