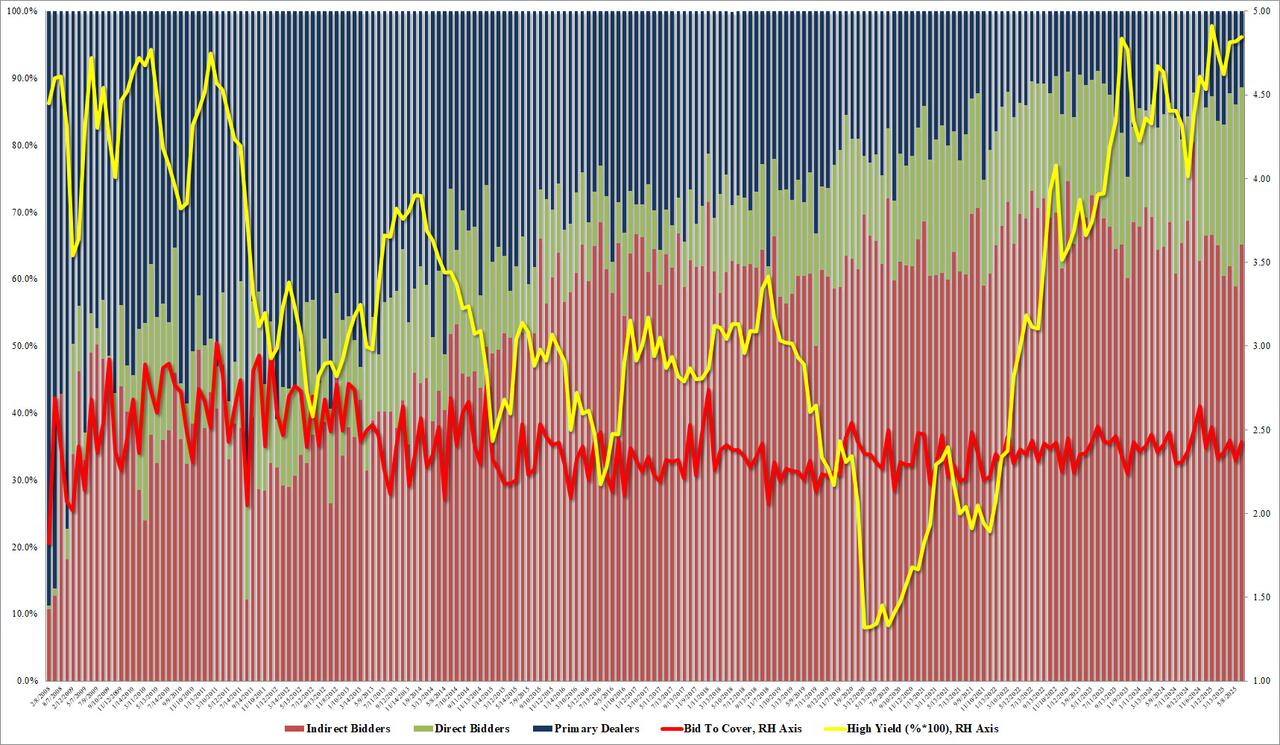

After a medicore 3Y auction to start the week, a solid 10Y auction yesterday, jittery traders were left with just one Treasury sale this week, arguably the most challenging one: today’s $25BN 30Y auction. In retrospect, there was no reason to worry because demand for today’s paper – especially among foreign buyers – was stellar any way you look at it.

Let’s take a look: starting at the top, the auction priced at a high yield of 4.844%, up from 4.819% last month and the highest since January; more importantly the auction stopped through the When Issued 4.859% by a solid 1.5bps, a reversal to last month’s 2.6 bps, and the second biggest through since November.

The bid to cover rose to 2.430 from last month’s 2.314, was the second highest since January which also put it above the six-auction average of 2.392.

The internals were even more impressive: foreign demand was solid with Indirects awarded 65.2%, up from 58.9% and the highest since January. And with Directs taking down 23.4%, down from 27.2% if above the recent average of 22.3%, Dealers were left with just 11.4$, the lowest since November as there was little need for them to step in considering solid demand.

The market response was favorable, with 10Y yields dropping near session lows of 4.34% – below where the 10Y traded ahead of last week’s solid NFP report – before retracing some of the move, because today’s auction notwithstanding, the US is still facing an avalanche of long duration to find Trump’s Big, Beautiful Bill.

Tyler Durden

Thu, 06/12/2025 – 13:29

Click this link for the original source of this article.

Author: Tyler Durden

This content is courtesy of, and owned and copyrighted by, https://zerohedge.com and its author. This content is made available by use of the public RSS feed offered by the host site and is used for educational purposes only. If you are the author or represent the host site and would like this content removed now and in the future, please contact USSANews.com using the email address in the Contact page found in the website menu.